$PMET

Canadian lithium miner.

Financials (USD):

- MC 319M, 245M

- Rev / net income / cash flow: NA, feasibility stage.

Management:

- Legendary CEO Ken Brindsen from Pilbara, who moved from Australia to Canada to lead the development. He took Pilbara through development from 250M to 16B MC.

- CEO has options for 1 million shares at $7 CAD and $9 CAD – provide targets in a follow the money thought process. Expiry August 2026.

Thesis:

- Canadian mine will be largest in the Americas, and 8th largest in the world.

- Currently lithium spodumene 6% price in the $600 range.

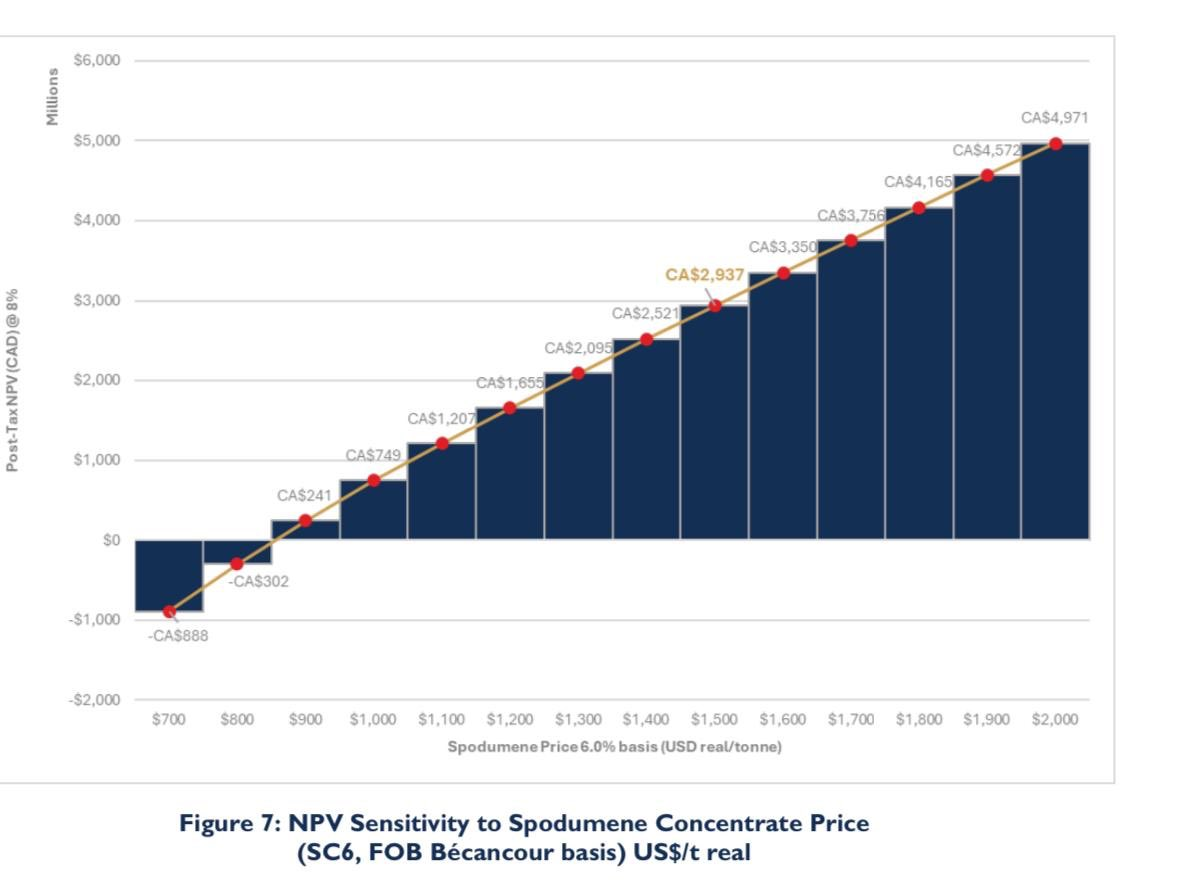

- PMET base case is $1500 long term, is this fair for mid cycle???

- Counter cyclical opportunity on price.

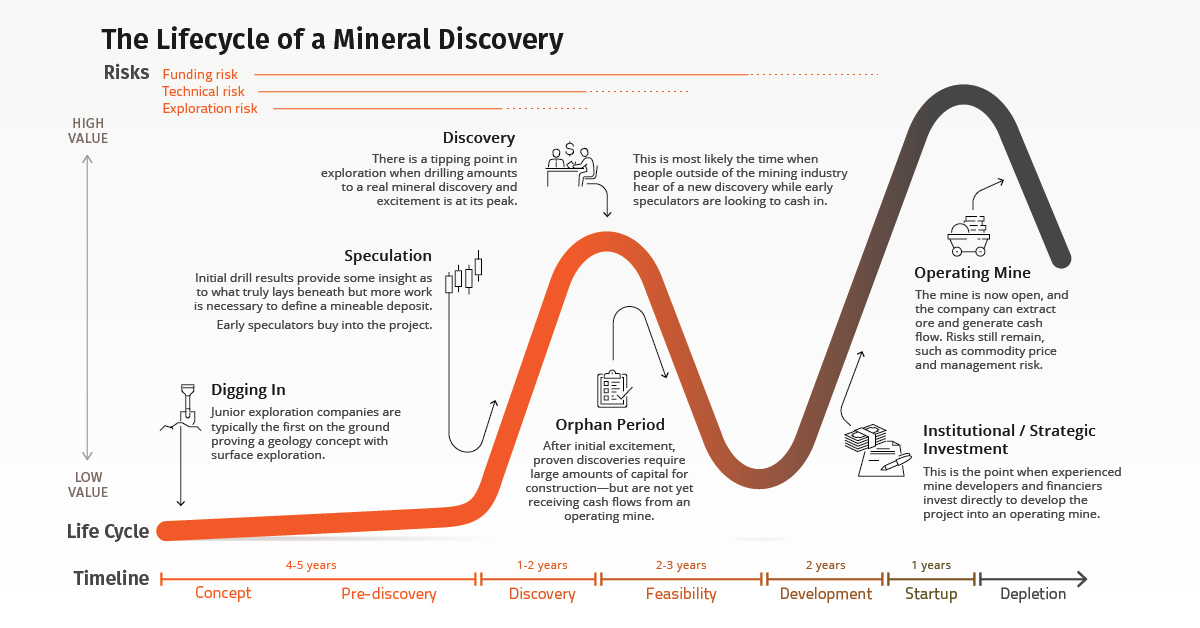

- Feasibility stage is typically a price downswing for any producer until development starts on Lassonde curve (middle down below). This can last for years. Construction expected in 2028 / production 2029 so this may take significant time. Feasibility study estimated completion Q3 2025.

- Volkswagon bought 10% at $4.50 CAD. Their first ever mining investment.

- Rare element finds, cesium found on property, at rare scale. Also, 4th largest tantalum deposit in the world.

- BESS optionality: Battery storage increasing lithium demand outside of auto. Thought to be something not all investors are watching.

Upside potential:

- 10x, back to prior highs. We are in the feasibility downslope at same time as a commodity pullback. Double double counter cyclical in a way. Chart below shows at 1500$/ton price its a 3B present value on the mine. 12x from here.

- Premium for North American?

- Cesium find, value add. Tantalum value.

Track prices: https://x.com/LithiumPriceBot

Risk/downside potential:

- Catching a falling knife still to a degree. Should find base here id think though.

- Opportunity risk of not playing tech and defense stocks on way up.

- What stops China from continuing to subsidize supply chain and make it uneconomical to west. This becomes a timing risk, as it could continue years.

- Good take on China angle, and why its not sustainable forever: https://x.com/sparkes_dwayne/status/1743122465629552677

https://x.com/sparkes_dwayne/status/1933350197196927393

- Good take on China angle, and why its not sustainable forever: https://x.com/sparkes_dwayne/status/1743122465629552677

Decision: Purchase entry level position, with plan to add more.